- In the build-up to the December 2019 UK General Election, the Conservative party made a manifesto pledge that ‘our world-leading offshore wind industry will reach 40GW by 2030’

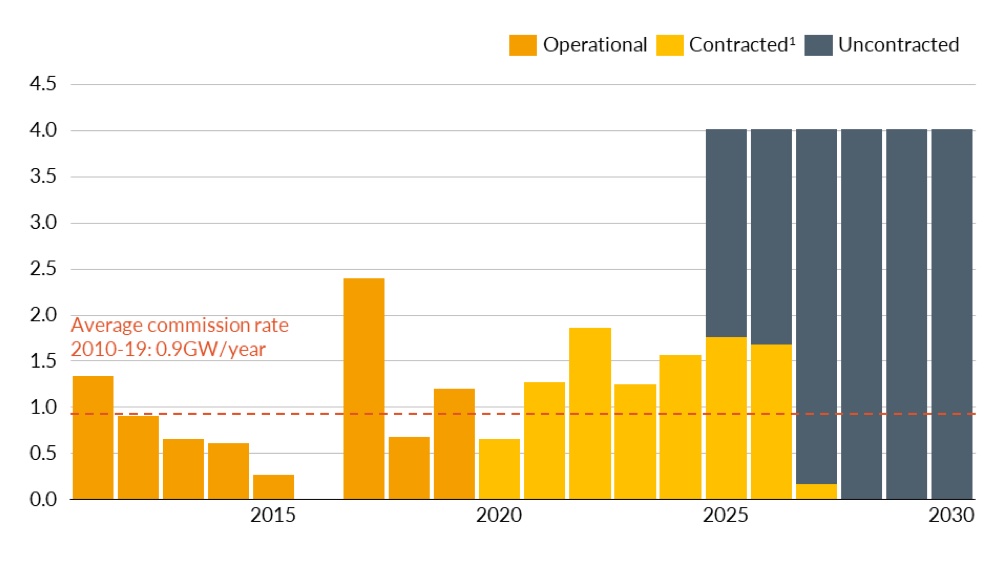

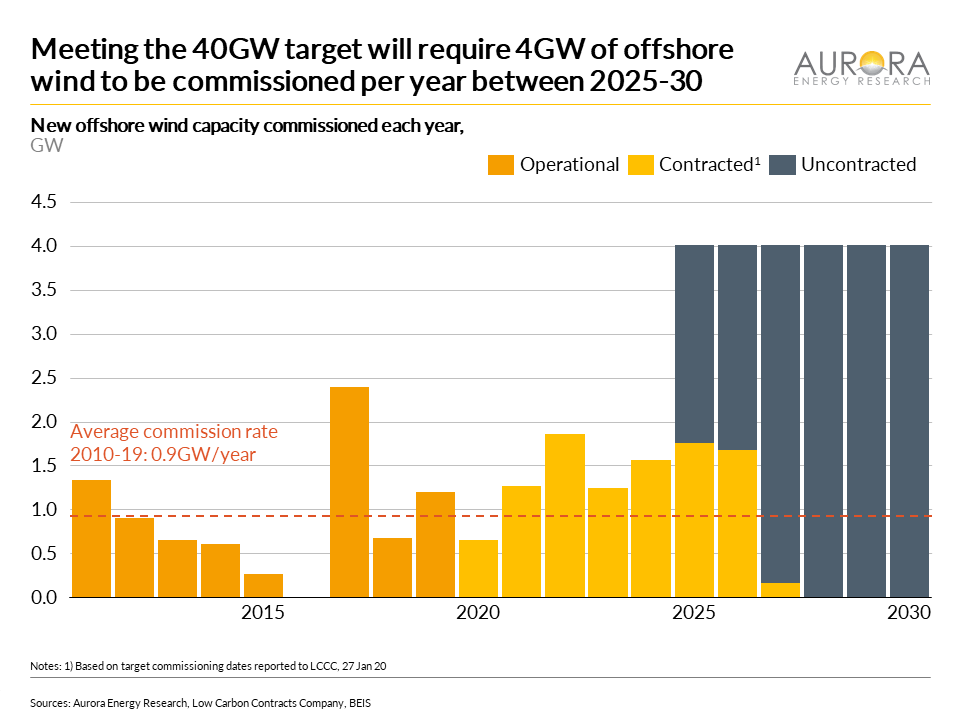

- Analysis by Aurora Energy Research shows that reaching the 40GW by 2030 target will require 30GW of capacity to be commissioned during the 2020s- three times as much as that installed during the 2010s. This would require one turbine to be installed every weekday during the whole of the 2020s, and almost £50bn in capital investment

- Increasing installed capacity to 40GW would cost a further £2.6bn per year in Contract for Difference top up payments – almost five times the allocated budget

New analysis by Aurora Energy Research – the leading energy market analytics and modelling firm – suggests that meeting the Government’s stated 40GW of offshore wind by 2030 target represents a major challenge for the industry and if achieved will have significant effects on the GB power market.

The UK’s offshore wind capacity has grown from 1GW in 2010 to almost 10GW at the start of 2020. In June 2019, the UK government committed to reaching net zero greenhouse gas emissions by 2050. Low carbon generation, such as offshore wind, is expected to play a vital role in reaching this target. In the build-up to the December 2019 UK General Election, the Conservative party made a manifesto pledge that ‘our world-leading offshore wind industry will reach 40GW by 2030’. At the commencement of the new parliament the Queen’s Speech again reaffirmed the 40GW by 2030 ambition. Other groups have pushed for even higher targets: the Labour party previously targeted 52GW by 2030; whilst Greenpeace recommended 45GW by 2030.

In order to meet the 40GW of offshore wind by 2030 target a number of challenges need to be overcome, both at a supply chain and investment level. To meet 40GW of offshore wind by 2030, an average annual installation rate of 260 turbines will need to be sustained over 5 years – equivalent to one turbine installed every weekday throughout the whole of the 2020s. This assumes that the turbines installed will also be three times larger than those installed between 2011-15, at 10-12MW per turbine. Almost 10GW of offshore wind capacity has already been contracted to come online during the 2020s. An additional 20GW of capacity will need to be procured through the Contract for Difference scheme, of which 17GW is yet to receive full planning consent.

Furthermore, the level of investment required is a steep increase from historic levels. £48bn of investment is estimated to be required during the 2020s to reach the 40GW target. This is twice as much as the estimated £24bn (real 2018 prices) invested into offshore wind during the 2010s.

Meeting this target would be a challenge for the industry but would create new green jobs in the UK and set the supply chain in good stead to export expertise beyond the UK’s market. However, higher levels of offshore wind will have a number of impacts on GB’s electricity markets:

- Lower capture prices for renewables which will in turn increase the payments made to both existing and future CfD supported projects – including renewables and nuclear. Assuming future offshore wind projects secure an average strike price of £40/MWh (2012 prices) the cost of reaching 40GW of CfDs would be a further £2.6bn (2012 prices) per year – almost five times the current budget of £557m

- Lower baseload prices which would reduce the total cost of the wholesale market to consumers

- Higher capacity market prices would have an upwards impact on total system cost. Prices will be higher due to the increase revenue that plants will require to stay economic in the face of lower wholesale revenue

Through the increasing level of subsidised offshore wind in the system, these factors combine to represent larger Government intervention in the power markets and reduce the amount of capacity which is exposed to purely market forces. This may put at risk onshore wind and solar PV projects which developers are attempting to bring forward on a fully merchant basis without direct Government support.

Martin Anderson, Head of GB Renewables at Aurora Energy Research and co-author of the report commented:

[1] Residual demand is defined here as total power demand minus output from renewables and nuclear“The Government’s 40GW target sets GB’s energy sector on a pathway towards the wider ambition of becoming net zero by 2050. Our analysis suggests that meeting this target will require a huge increase in the deployment rate of offshore wind turbines, alongside significant capital investment, and planning consents to be approved in record time. Whilst offshore wind has demonstrated significant cost reductions in previous auctions, the impact of higher levels of renewables in the system will reduce offshore wind capture prices and the subsidy support schemes will require further budget. Should this target be achieved it would have wide implications for existing investors in the GB power system and represent significant Government involvement into the liberalised electricity markets.”

Media contact

Caroline Oates

Marketing and Media Associate

E: caroline.oates@auroraer.com

T: +44 (0)1865 952700

M:+44 (0)7912 568570

Martin Anderson

Head of GB Renewables

E: martin.anderson@auroraer.com

Notes to editors

Aurora Energy Research is a leading independent European energy market analytics company founded in 2013 by University of Oxford professors and economists. Aurora provides deep insights into European and global energy markets supported by cutting edge models to help our clients navigate the global energy transition and make bankable investment decisions. We work with world leading organisations across Europe, including energy companies, financial institutions and governments. Our services include: subscription-based forecasts, reports, forums and bespoke consultancy services. Aurora Energy Research has offices in Oxford, Berlin and Sydney. For further information, please visit auroraer.com